Guides

ประกันสำหรับคอนโดให้เช่า: เจ้าของต้องทำหรือไม่

Protect your rental property and finances with the right insurance coverage.

Summary

ประกันคอนโดให้เช่า is essential for property owners. Learn what coverage you need, costs, and how to protect your investment from risks.

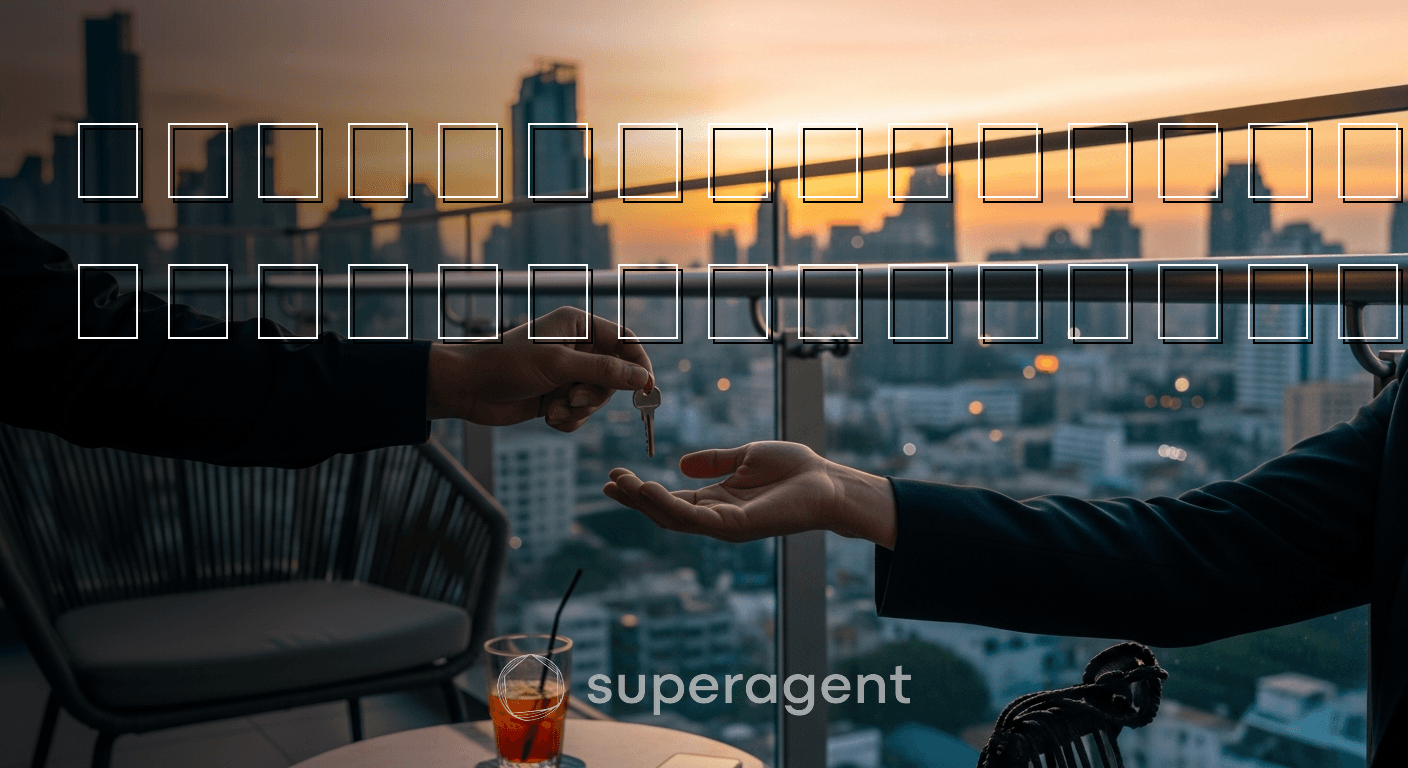

You just bought a condo near BTS Thong Lo. You found a tenant paying 35,000 THB per month. Everything looks great until a pipe bursts in the unit, flooding the kitchen and damaging your built-in cabinets. The repair bill comes to 120,000 THB. Your tenant says it is not their fault. You check your juristic person's common area insurance and realize it does not cover anything inside your unit. Now what? This is exactly the kind of situation that makes condo rental insurance worth thinking about seriously, especially if you are renting out property in Bangkok.

What Is Condo Rental Insurance and Why Should Bangkok Landlords Care?

Condo rental insurance is a policy that protects property owners from financial losses related to renting out their unit. It can cover damage to the property, liability if someone gets injured in your unit, loss of rental income, and even legal expenses if a dispute with a tenant goes sideways.

Here is the thing most Bangkok landlords get wrong. They assume the building's master insurance policy covers their individual unit. It does not. The juristic person's insurance typically covers common areas like lobbies, pools, and elevators. Everything inside your four walls, from air conditioning units to flooring to furniture, is your responsibility.

According to CBRE Thailand's market research, Bangkok's condo rental market continues to attract both local and international investors, with average yields hovering around 4 to 5 percent for well-located units. That yield disappears fast when you are hit with an uninsured loss. A landlord renting out a furnished one-bedroom at Life Asoke Hype near MRT Phetchaburi for 22,000 THB per month could lose six months of rental income from a single uninsured water damage incident.

The short answer to whether you must have insurance is no, Thai law does not require landlords to carry rental property insurance. But the smarter question is whether you can afford not to.

What Does Condo Rental Insurance Actually Cover?

Not all policies are created equal, and coverage varies between Thai insurers. But most landlord-focused property insurance policies available in Thailand will cover a combination of the following.

Property damage is the big one. This includes fire, water damage, storms, and sometimes theft. If you are renting out a furnished unit in a building like Ideo Q Sukhumvit 36 near BTS Thong Lo, you probably have 300,000 to 500,000 THB worth of furniture and appliances inside. One electrical fire and that investment is gone without coverage.

Liability protection covers you if a tenant or their guest gets injured in your unit. Say a glass shower panel shatters and injures someone. Without liability coverage, you could be looking at medical bills and potential legal action. Bumrungrad Hospital is excellent, but a visit there is not cheap.

Loss of rental income is another valuable component. If your unit becomes uninhabitable due to a covered event, some policies will compensate you for the rent you lose while repairs are being made. For a two-bedroom at Ashton Asoke near MRT Sukhumvit renting at 45,000 THB per month, even two months of lost rent adds up to 90,000 THB.

Some policies also cover tenant-caused damage beyond the security deposit, legal expenses for eviction proceedings, and even contents insurance if you are renting the unit fully furnished.

How Much Does It Cost and Is It Worth It?

This is where the math gets interesting. Annual premiums for landlord insurance on a Bangkok condo typically range from 3,000 to 15,000 THB per year, depending on coverage limits, the value of the property and contents, and the location of the building.

Let me put that in perspective. If you own a one-bedroom condo near BTS Ari that rents for 18,000 THB per month, your annual rental income is 216,000 THB. An insurance premium of 5,000 THB per year represents roughly 2.3 percent of your gross rental income. That is a small price for peace of mind.

A real scenario that plays out constantly in Bangkok: a tenant at a mid-range condo on Soi Sukhumvit 49 leaves the air conditioning running while away for a long weekend. The drain pan overflows, water seeps into the floor, and the laminate warping damage costs 80,000 THB to repair. The security deposit was only two months at 25,000 THB each, so 50,000 THB. The landlord is still 30,000 THB in the hole, and good luck recovering that from a tenant who may have already left the country.

According to data from Knight Frank Thailand, the average insured value of contents in a furnished Bangkok rental condo ranges from 200,000 to 800,000 THB. When you weigh a potential loss of that magnitude against an annual premium under 15,000 THB, the decision becomes pretty straightforward.

Types of Insurance Policies Bangkok Landlords Should Know About

There are several types of insurance products available in Thailand that are relevant to condo landlords. Understanding the differences will help you pick the right coverage.

Standard fire insurance is the most basic option. It covers fire, lightning, and explosion. This is the minimum that most mortgage lenders require, but it leaves huge gaps. It will not cover water damage, theft, or liability.

Comprehensive property insurance, sometimes called all-risk insurance, is a much better fit for landlords. It covers a wider range of events including water damage, storms, vehicle impact, and sometimes even terrorism. Most major Thai insurers like Viriyah, Bangkok Insurance, and Dhipaya offer versions of this.

Landlord-specific insurance is harder to find in Thailand compared to markets like the UK or Australia, but some international insurers and brokers operating in Bangkok do offer tailored landlord policies. These bundle property coverage with liability, rental loss, and legal expense coverage.

Consider a landlord who owns two units at The Base Park West near BTS On Nut, renting each at 15,000 THB per month. With combined annual rental income of 360,000 THB, spending 10,000 to 20,000 THB on comprehensive coverage for both units is a rational business expense.

| Insurance Type | Annual Premium Range (THB) | Typical Coverage | Best For |

|---|---|---|---|

| Standard Fire Insurance | 1,500 to 4,000 | Fire, lightning, explosion only | Minimum mortgage requirement |

| Comprehensive Property Insurance | 3,000 to 10,000 | Fire, water, storm, theft, all-risk | Unfurnished or lightly furnished units |

| Landlord-Specific Policy | 8,000 to 15,000 | Property, liability, rental loss, legal costs | Fully furnished rental condos |

| Contents-Only Insurance | 2,000 to 6,000 | Furniture, appliances, electronics | Add-on for furnished units |

Common Mistakes Bangkok Landlords Make with Insurance

The biggest mistake is simply not having any coverage at all. A surprising number of landlords in Bangkok, especially those who bought investment condos in areas like Ratchada or Rama 9, skip insurance entirely because they see it as an unnecessary cost. They are essentially self-insuring against risks they may not be able to absorb.

Another common error is underinsuring the contents. If you furnished your two-bedroom unit at Rhythm Sukhumvit 36-38 near BTS Thong Lo with 400,000 THB worth of furniture but only insured contents for 100,000 THB, you are going to be very disappointed when you file a claim.

Some landlords also confuse their tenant's renter insurance with their own coverage. These are two completely different things. A tenant's renter policy covers the tenant's personal belongings. It does not cover your built-in kitchen, your sofa, or the damage the tenant causes to your property. As a landlord, you need your own policy.

A common scenario on Soi Sukhumvit 24: a landlord rents a furnished studio to an expat for 20,000 THB per month. The tenant accidentally starts a small grease fire in the kitchen. The damage totals 60,000 THB. The tenant's renter insurance covers their laptop and clothes. The landlord's kitchen cabinets, countertop, and microwave? That is all on the landlord without proper coverage.

Tax Implications and Deductibility for Landlords

Here is a detail that many Bangkok landlords overlook. Insurance premiums on rental properties can potentially be claimed as a deductible expense against your rental income when filing taxes with the Thai Revenue Department.

If you choose the actual expense deduction method rather than the standard deduction of 30 percent for rental income, your insurance premiums, along with maintenance costs, management fees, and depreciation, can reduce your taxable rental income. For landlords with multiple units or higher-value properties, this can make a meaningful difference.

For example, a landlord earning 540,000 THB per year from renting a two-bedroom at Magnolias Waterfront Residences at ICONSIAM near BTS Krung Thon Buri could deduct insurance premiums, common area fees, and repair costs if they exceed the standard 30 percent deduction of 162,000 THB. This is worth discussing with a Thai tax accountant to find the most advantageous approach for your situation.

The bottom line is this. Thai law does not force you to buy insurance for your rental condo. But if you are treating your condo as an investment, and you should be, then insurance is simply a cost of doing business. The premiums are modest compared to the potential losses. A single water damage incident, liability claim, or extended vacancy due to repairs can wipe out a full year of rental income. For a few thousand baht a year, you protect your asset, your income stream, and your peace of mind. That is a deal most savvy Bangkok landlords would take every time.

If you are looking for tenants for your insured and well-maintained condo, or if you are a renter searching for quality units from responsible landlords, check out superagent.co. Superagent uses AI to match tenants with the right condos across Bangkok, making the rental process smoother for everyone involved.

You just bought a condo near BTS Thong Lo. You found a tenant paying 35,000 THB per month. Everything looks great until a pipe bursts in the unit, flooding the kitchen and damaging your built-in cabinets. The repair bill comes to 120,000 THB. Your tenant says it is not their fault. You check your juristic person's common area insurance and realize it does not cover anything inside your unit. Now what? This is exactly the kind of situation that makes condo rental insurance worth thinking about seriously, especially if you are renting out property in Bangkok.

What Is Condo Rental Insurance and Why Should Bangkok Landlords Care?

Condo rental insurance is a policy that protects property owners from financial losses related to renting out their unit. It can cover damage to the property, liability if someone gets injured in your unit, loss of rental income, and even legal expenses if a dispute with a tenant goes sideways.

Here is the thing most Bangkok landlords get wrong. They assume the building's master insurance policy covers their individual unit. It does not. The juristic person's insurance typically covers common areas like lobbies, pools, and elevators. Everything inside your four walls, from air conditioning units to flooring to furniture, is your responsibility.

According to CBRE Thailand's market research, Bangkok's condo rental market continues to attract both local and international investors, with average yields hovering around 4 to 5 percent for well-located units. That yield disappears fast when you are hit with an uninsured loss. A landlord renting out a furnished one-bedroom at Life Asoke Hype near MRT Phetchaburi for 22,000 THB per month could lose six months of rental income from a single uninsured water damage incident.

The short answer to whether you must have insurance is no, Thai law does not require landlords to carry rental property insurance. But the smarter question is whether you can afford not to.

What Does Condo Rental Insurance Actually Cover?

Not all policies are created equal, and coverage varies between Thai insurers. But most landlord-focused property insurance policies available in Thailand will cover a combination of the following.

Property damage is the big one. This includes fire, water damage, storms, and sometimes theft. If you are renting out a furnished unit in a building like Ideo Q Sukhumvit 36 near BTS Thong Lo, you probably have 300,000 to 500,000 THB worth of furniture and appliances inside. One electrical fire and that investment is gone without coverage.

Liability protection covers you if a tenant or their guest gets injured in your unit. Say a glass shower panel shatters and injures someone. Without liability coverage, you could be looking at medical bills and potential legal action. Bumrungrad Hospital is excellent, but a visit there is not cheap.

Loss of rental income is another valuable component. If your unit becomes uninhabitable due to a covered event, some policies will compensate you for the rent you lose while repairs are being made. For a two-bedroom at Ashton Asoke near MRT Sukhumvit renting at 45,000 THB per month, even two months of lost rent adds up to 90,000 THB.

Some policies also cover tenant-caused damage beyond the security deposit, legal expenses for eviction proceedings, and even contents insurance if you are renting the unit fully furnished.

How Much Does It Cost and Is It Worth It?

This is where the math gets interesting. Annual premiums for landlord insurance on a Bangkok condo typically range from 3,000 to 15,000 THB per year, depending on coverage limits, the value of the property and contents, and the location of the building.

Let me put that in perspective. If you own a one-bedroom condo near BTS Ari that rents for 18,000 THB per month, your annual rental income is 216,000 THB. An insurance premium of 5,000 THB per year represents roughly 2.3 percent of your gross rental income. That is a small price for peace of mind.

A real scenario that plays out constantly in Bangkok: a tenant at a mid-range condo on Soi Sukhumvit 49 leaves the air conditioning running while away for a long weekend. The drain pan overflows, water seeps into the floor, and the laminate warping damage costs 80,000 THB to repair. The security deposit was only two months at 25,000 THB each, so 50,000 THB. The landlord is still 30,000 THB in the hole, and good luck recovering that from a tenant who may have already left the country.

According to data from Knight Frank Thailand, the average insured value of contents in a furnished Bangkok rental condo ranges from 200,000 to 800,000 THB. When you weigh a potential loss of that magnitude against an annual premium under 15,000 THB, the decision becomes pretty straightforward.

Types of Insurance Policies Bangkok Landlords Should Know About

There are several types of insurance products available in Thailand that are relevant to condo landlords. Understanding the differences will help you pick the right coverage.

Standard fire insurance is the most basic option. It covers fire, lightning, and explosion. This is the minimum that most mortgage lenders require, but it leaves huge gaps. It will not cover water damage, theft, or liability.

Comprehensive property insurance, sometimes called all-risk insurance, is a much better fit for landlords. It covers a wider range of events including water damage, storms, vehicle impact, and sometimes even terrorism. Most major Thai insurers like Viriyah, Bangkok Insurance, and Dhipaya offer versions of this.

Landlord-specific insurance is harder to find in Thailand compared to markets like the UK or Australia, but some international insurers and brokers operating in Bangkok do offer tailored landlord policies. These bundle property coverage with liability, rental loss, and legal expense coverage.

Consider a landlord who owns two units at The Base Park West near BTS On Nut, renting each at 15,000 THB per month. With combined annual rental income of 360,000 THB, spending 10,000 to 20,000 THB on comprehensive coverage for both units is a rational business expense.

Talk to us about renting

Share your details and keep reading — we’ll get back to you.

| Insurance Type | Annual Premium Range (THB) | Typical Coverage | Best For |

|---|---|---|---|

| Standard Fire Insurance | 1,500 to 4,000 | Fire, lightning, explosion only | Minimum mortgage requirement |

| Comprehensive Property Insurance | 3,000 to 10,000 | Fire, water, storm, theft, all-risk | Unfurnished or lightly furnished units |

| Landlord-Specific Policy | 8,000 to 15,000 | Property, liability, rental loss, legal costs | Fully furnished rental condos |

| Contents-Only Insurance | 2,000 to 6,000 | Furniture, appliances, electronics | Add-on for furnished units |

Common Mistakes Bangkok Landlords Make with Insurance

The biggest mistake is simply not having any coverage at all. A surprising number of landlords in Bangkok, especially those who bought investment condos in areas like Ratchada or Rama 9, skip insurance entirely because they see it as an unnecessary cost. They are essentially self-insuring against risks they may not be able to absorb.

Another common error is underinsuring the contents. If you furnished your two-bedroom unit at Rhythm Sukhumvit 36-38 near BTS Thong Lo with 400,000 THB worth of furniture but only insured contents for 100,000 THB, you are going to be very disappointed when you file a claim.

Some landlords also confuse their tenant's renter insurance with their own coverage. These are two completely different things. A tenant's renter policy covers the tenant's personal belongings. It does not cover your built-in kitchen, your sofa, or the damage the tenant causes to your property. As a landlord, you need your own policy.

A common scenario on Soi Sukhumvit 24: a landlord rents a furnished studio to an expat for 20,000 THB per month. The tenant accidentally starts a small grease fire in the kitchen. The damage totals 60,000 THB. The tenant's renter insurance covers their laptop and clothes. The landlord's kitchen cabinets, countertop, and microwave? That is all on the landlord without proper coverage.

Tax Implications and Deductibility for Landlords

Here is a detail that many Bangkok landlords overlook. Insurance premiums on rental properties can potentially be claimed as a deductible expense against your rental income when filing taxes with the Thai Revenue Department.

If you choose the actual expense deduction method rather than the standard deduction of 30 percent for rental income, your insurance premiums, along with maintenance costs, management fees, and depreciation, can reduce your taxable rental income. For landlords with multiple units or higher-value properties, this can make a meaningful difference.

For example, a landlord earning 540,000 THB per year from renting a two-bedroom at Magnolias Waterfront Residences at ICONSIAM near BTS Krung Thon Buri could deduct insurance premiums, common area fees, and repair costs if they exceed the standard 30 percent deduction of 162,000 THB. This is worth discussing with a Thai tax accountant to find the most advantageous approach for your situation.

The bottom line is this. Thai law does not force you to buy insurance for your rental condo. But if you are treating your condo as an investment, and you should be, then insurance is simply a cost of doing business. The premiums are modest compared to the potential losses. A single water damage incident, liability claim, or extended vacancy due to repairs can wipe out a full year of rental income. For a few thousand baht a year, you protect your asset, your income stream, and your peace of mind. That is a deal most savvy Bangkok landlords would take every time.

If you are looking for tenants for your insured and well-maintained condo, or if you are a renter searching for quality units from responsible landlords, check out superagent.co. Superagent uses AI to match tenants with the right condos across Bangkok, making the rental process smoother for everyone involved.

Share this article

Properties you may like

![[For Rent] BUILDING I Quach House Phrom Phong I 1st-6th Floor I 100,000-135,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F1976%2F333d3ec9-941e-431d-8a0c-68b9d7bdbc41-1000002210.jpg&w=3840&q=75)

฿135,000

[For Rent] BUILDING I Quach House Phrom Phong I 1st-6th Floor I 100,000-135,000THB/mo

Townhouse![[For Rent] CONDO I Waterford Diamond Sukhumvit 30/1 I 3 Beds I 3 Baths I 65,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2049%2Fa78ddba5-043d-459a-97eb-4f80a7bf7d1a-8f2dc5c8-f220-47ae-b027-7deab6c6666b-media.jpg&w=3840&q=75)

฿65,000

[For Rent] CONDO I Waterford Diamond Sukhumvit 30/1 I 3 Beds I 3 Baths I 65,000THB/mo

Phrom Phong

Condo![[For Rent] HOUSE I Centro Vibhavadi I 4 Beds I 3 Baths I 80,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2048%2F7bcb9b3f-6bca-4615-8451-eb71e0910ecc-26-07-09-15-10-22-747_deco.jpg&w=3840&q=75)

฿80,000

[For Rent] HOUSE I Centro Vibhavadi I 4 Beds I 3 Baths I 80,000THB/mo

House![[For Rent] CONDO I RHYTHM Sathorn I 1 Bed I 1 Bath I 20,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2045%2Fcd83dbf6-1fcd-43e1-9788-a9f9ef92106c-img_2861.jpg&w=3840&q=75)

฿20,000

[For Rent] CONDO I RHYTHM Sathorn I 1 Bed I 1 Bath I 20,000THB/mo

Condo![[For Rent] TOWNHOME I Gravitia Rama 2-Thakam I 3 Beds I 3 Baths I 35,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2046%2F3a6c0105-9e14-456f-8fde-b8a52d7cec89-line_album_-531_260714_16.jpg&w=3840&q=75)

฿35,000

[For Rent] TOWNHOME I Gravitia Rama 2-Thakam I 3 Beds I 3 Baths I 35,000THB/mo

Townhouse![[For Rent & Sale] CONDO I KHUN by YOO I 2 Beds I 2 Baths I Rent 130,000THB/mo - Sale 37,000,000mb THB](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2015%2Fac778d88-63d8-418e-8291-ce27e76eb87b-17227fa8597d930453882fcb8eceab768aa7d514.jpg&w=3840&q=75)

฿130,000

[For Rent & Sale] CONDO I KHUN by YOO I 2 Beds I 2 Baths I Rent 130,000THB/mo - Sale 37,000,000mb THB

Thonglor

Condo![[For Rent] CONDO I IDEO Ratchada-Huai Khwang I 2 Beds I 2 Baths I 25,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F1935%2Fac9ba95a-0ad4-4121-9287-226c06205f6f-1782609678044-61071c89.jpg&w=3840&q=75)

฿25,000

[For Rent] CONDO I IDEO Ratchada-Huai Khwang I 2 Beds I 2 Baths I 25,000THB/mo

Huai Khwang

Condo![[For Rent] HOUSE I Laddarom Rattanathibet I 4 Beds I 3 Baths I Rent 80,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2035%2Ff8ee11b5-97d3-475e-b58b-49ebc833161e-ef77c7dc-87f5-4b5e-8a7d-0c4e41b65b6b-a34.jpg&w=3840&q=75)

฿80,000

[For Rent] HOUSE I Laddarom Rattanathibet I 4 Beds I 3 Baths I Rent 80,000THB/mo

House![[For Rent] CONDO I Life @ Sathon 10 I 1 Bed I 1 Bath I Rent 20,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F1954%2F3e4ff511-b8de-40a5-894e-c8fc6777e2b0-living-room1.jpg&w=3840&q=75)

฿20,000

[For Rent] CONDO I Life @ Sathon 10 I 1 Bed I 1 Bath I Rent 20,000THB/mo

Sathorn

Condo![[For Rent&Sale] CONDO I Belle Grand Rama 9 I 2 Beds I 2 Baths I Rent 45,000THB/mo - Sale 10.7mb THB](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F1961%2Fef57f38f-f765-4980-a394-8c66e43efea4-line_album_27626_260701_11.jpg&w=3840&q=75)

฿45,000

[For Rent&Sale] CONDO I Belle Grand Rama 9 I 2 Beds I 2 Baths I Rent 45,000THB/mo - Sale 10.7mb THB

CondoMore like this

In Guides · Superagent EditorialHidden Costs of Renting a Condo in Bangkok Nobody Warns You AboutBangkok condo rent looks affordable until month one hits. Here are the real costs beyond the headline figure that catch most renters off guard.25 May 20261 min read

In Guides · Superagent EditorialHidden Costs of Renting a Condo in Bangkok Nobody Warns You AboutBangkok condo rent looks affordable until month one hits. Here are the real costs beyond the headline figure that catch most renters off guard.25 May 20261 min read In Guides · Superagent EditorialWhat a Long-Vacant Bangkok Condo Unit Is Actually Telling YouA Bangkok condo vacant for months signals overpricing, landlord issues, or real problems. Here is how to read the signs.25 May 20261 min read

In Guides · Superagent EditorialWhat a Long-Vacant Bangkok Condo Unit Is Actually Telling YouA Bangkok condo vacant for months signals overpricing, landlord issues, or real problems. Here is how to read the signs.25 May 20261 min read In Guides · Superagent EditorialRed Flags in a Bangkok Rental Contract to Watch Out ForBangkok rental contracts often hide risky clauses. Here are the red flags every tenant must catch before signing any lease.25 May 20261 min read

In Guides · Superagent EditorialRed Flags in a Bangkok Rental Contract to Watch Out ForBangkok rental contracts often hide risky clauses. Here are the red flags every tenant must catch before signing any lease.25 May 20261 min read In Guides · Superagent EditorialWorking Online from a Condo: How to Choose the Perfect Room for ProductivityLearn how to choose the best condo room for working online with tips on lighting, noise, and furniture setup to maximize productivity.9 May 20261 min read

In Guides · Superagent EditorialWorking Online from a Condo: How to Choose the Perfect Room for ProductivityLearn how to choose the best condo room for working online with tips on lighting, noise, and furniture setup to maximize productivity.9 May 20261 min read