Guides

ประกันสำหรับคอนโดให้เช่า: เจ้าของควรซื้อแบบไหน

Protect your rental investment with the right condo insurance policy

Summary

ประกันภัยคอนโดให้เช่า ไทย offers essential coverage for rental property owners. Learn which insurance types protect your investment and tenants effectively

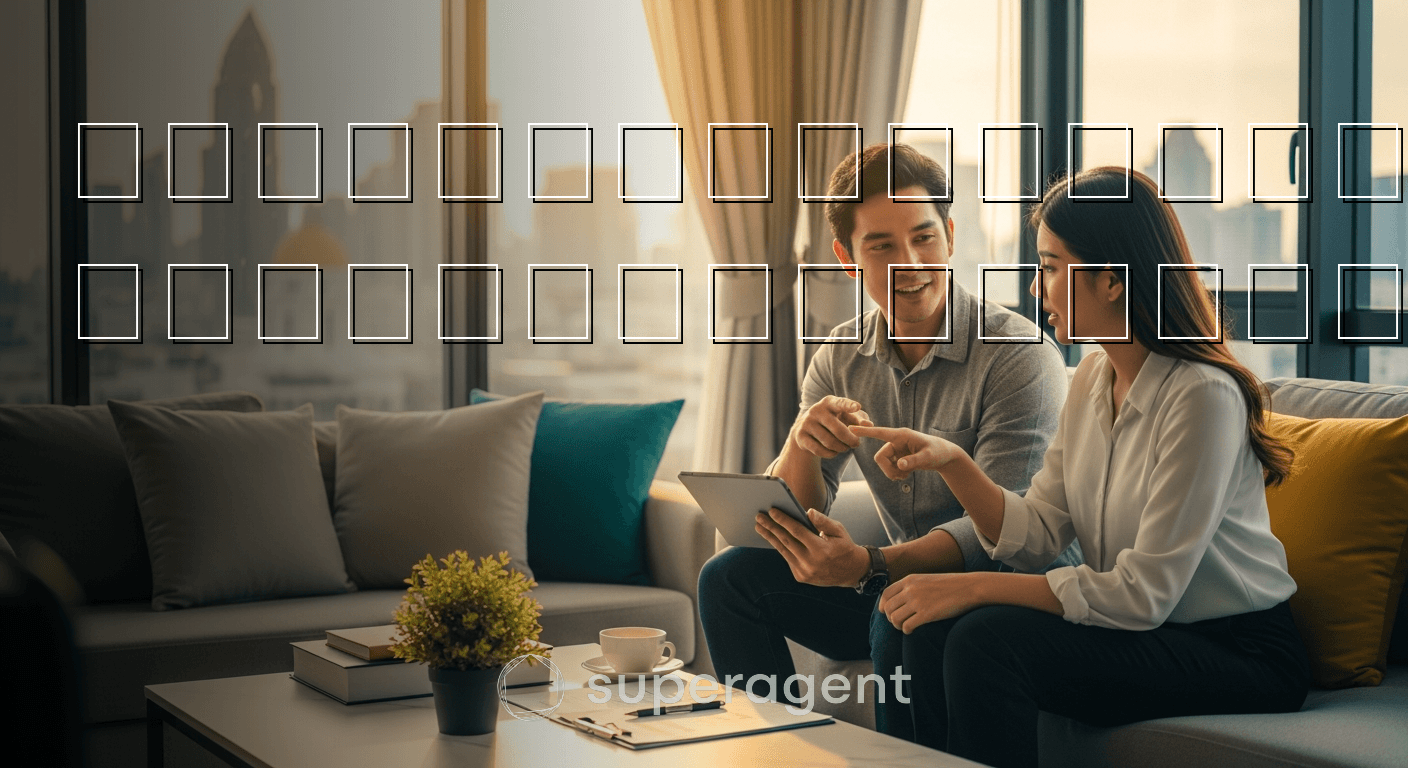

You bought a condo near BTS Thong Lo as an investment. You spent 4.5 million baht on a one-bedroom unit at The Lofts Ekkamai, renovated the kitchen, added nice furniture, and listed it for rent at 28,000 baht per month. Within two weeks, a tenant moved in. Everything felt great. Then three months later, a pipe burst inside the wall, flooded the unit, destroyed the wooden flooring, and ruined the tenant's laptop. The repair bill came to 180,000 baht. Your tenant wanted compensation. Your juristic person said the pipe was inside your unit, so it was your responsibility. And you had zero insurance. This is the scenario nobody thinks about until it happens. If you own a rental condo in Bangkok, insurance is not optional. It is one of the smartest, cheapest protections you can buy. Let's break down exactly what kind of insurance you need and why.

Why Most Bangkok Condo Landlords Skip Insurance

Here is the honest truth. Most condo owners in Thailand do not buy insurance for their rental units. They assume the building's master insurance policy covers everything. It does not. The juristic person's policy typically covers common areas like lobbies, pools, elevators, and the building's structural elements. It rarely covers anything inside your individual unit.

Think about a building like Life Asoke Hype near MRT Phetchaburi. The juristic office maintains insurance for the entire building structure, but if a fire starts in your kitchen because of a faulty electrical outlet, you are on the hook for damages inside your four walls. Your tenant's belongings, your furniture, the repaint, the new flooring. All of it comes out of your pocket.

According to CBRE Thailand, the average rental yield for condos in central Bangkok sits between 3.5% and 5.5% annually. One uninsured incident can wipe out two or three years of rental income. That is a risk no serious investor should take.

The Three Types of Insurance Every Rental Condo Owner Should Know

Insurance in Thailand for residential property is not as complicated as people think. There are essentially three categories that matter for landlords. Understanding the differences will save you from buying the wrong policy or, worse, buying nothing at all.

The first is fire insurance, which is the most basic. In Thailand, fire insurance policies are standardized by the Office of Insurance Commission (OIC) and cover fire, lightning, and explosion. Premiums are very affordable, often under 1,000 baht per year for a condo valued at 3 to 5 million baht. But fire insurance alone is limited. It does not cover water damage, theft, or third-party liability.

The second type is comprehensive property insurance, sometimes called all-risk or multi-peril insurance. This is the one most landlords should seriously consider. It covers fire, flooding, burst pipes, storm damage, theft, and sometimes even damage caused by tenants. For a rental condo in a building like Ideo Mobi Sukhumvit near BTS On Nut, renting at around 15,000 to 20,000 baht per month, a comprehensive policy might cost between 2,500 and 5,000 baht per year. That is less than one week of rental income for a full year of coverage.

The third type is liability insurance. This is the one almost nobody buys, but it can be the most important. Imagine your air conditioning unit leaks and damages the ceiling of the unit below yours. Or your tenant's guest slips on your wet bathroom floor and breaks a wrist. Liability insurance covers claims made against you as the property owner. Some comprehensive policies include basic liability coverage. Others require a separate rider.

What Does a Typical Policy Actually Cover?

Let's get specific. Say you own a one-bedroom condo at Aspire Sukhumvit 48 near BTS Phra Khanong. You rent it out furnished at 18,000 baht per month. You buy a comprehensive property insurance policy for 3,200 baht per year. Here is what that policy would typically cover and not cover.

| Coverage Area | Typically Covered | Usually Not Covered | Estimated Annual Premium Range |

|---|---|---|---|

| Fire and Explosion | Yes, including damage to structure and contents | Arson by the owner | 800 to 1,200 THB |

| Water Damage (burst pipes, leaks) | Yes, sudden and accidental | Gradual seepage or poor maintenance | Included in comprehensive |

| Flooding from Natural Events | Sometimes, with a specific rider | Often excluded in standard policies | 500 to 2,000 THB add-on |

| Theft and Burglary | Yes, with forced entry evidence | Theft by tenant or household member | Included in comprehensive |

| Tenant Damage (intentional) | Rarely covered | Deliberate destruction by tenant | Separate landlord policy needed |

| Third-Party Liability | Yes, if included or added as rider | Professional or business liability | 500 to 1,500 THB add-on |

| Loss of Rental Income | Yes, in premium policies | Vacancy due to market conditions | 1,000 to 3,000 THB add-on |

The key takeaway from this table is that a comprehensive policy costing 2,500 to 5,000 baht per year covers the most common risks a Bangkok landlord faces. That is roughly 0.07% to 0.1% of a condo's value. Compare that to the potential cost of a single water damage incident, which can easily run 100,000 baht or more, and the math is obvious.

Flooding Risk and Why Location Matters for Your Premium

Bangkok has a complicated relationship with water. The city sits barely above sea level, and certain neighborhoods flood more than others. If your rental condo is in a low-lying area like parts of Soi Lat Phrao or near the Chao Phraya river, your insurance premium for flood coverage will be higher, sometimes significantly.

Consider this scenario. You own a studio at a riverside condo like Supalai River Resort near BTS Saphan Taksin. The views are gorgeous, the rent is solid at around 12,000 to 16,000 baht per month, but the flood risk is real. During the 2011 floods, riverside properties took serious damage. Insurers remember this. A flood rider for a riverside condo might cost 2,000 to 4,000 baht per year, while the same rider for a unit at a high-rise on Sukhumvit Soi 24 might be half that.

According to data referenced by Knight Frank Thailand, properties in flood-prone zones can see insurance premiums 30% to 60% higher than comparable units in elevated, well-drained areas. This is worth factoring into your investment calculations, especially if you are comparing rental yields across different neighborhoods.

What About Tenant Damage and the Security Deposit?

This is where most landlords feel the most frustration. Your tenant moves out after a one-year lease at a condo like Rhythm Sukhumvit 36-38 near BTS Thong Lo. You walk in and find cigarette burns on the sofa, a cracked bathroom mirror, stains all over the curtains, and a missing microwave. The security deposit was two months at 25,000 baht per month, so you have 50,000 baht to work with. But the actual repair and replacement cost is 75,000 baht.

Standard property insurance does not cover intentional tenant damage. This is a gap that most policies explicitly exclude. Some Thai insurers now offer landlord-specific policies that cover tenant damage, but they are still uncommon and tend to carry higher premiums and deductibles. The more practical approach for most Bangkok landlords is to combine a solid comprehensive insurance policy with a well-drafted lease agreement that clearly outlines the tenant's responsibilities.

Your lease should include a detailed inventory checklist with photos, signed by both parties at move-in. This is your best protection against tenant damage disputes, even more effective than insurance in most cases. Use the security deposit strategically and document everything.

How to Choose the Right Insurance Provider in Thailand

Thailand has dozens of insurance companies, but not all of them handle condo property insurance well. The major players for residential property insurance include Viriyah Insurance, Bangkok Insurance, Dhipaya Insurance, and Muang Thai Insurance. All four are well-established, financially stable, and regulated by the OIC.

Here is a real-world example of how to approach this. Say you own two rental condos, a one-bedroom at Ideo Q Siam near BTS Ratchathewi renting at 22,000 baht per month and a studio at Lumpini Park Rama 9 near MRT Rama 9 renting at 11,000 baht per month. You would want comprehensive property insurance for both units. You can often get a discount by insuring multiple properties with the same company.

Start by requesting quotes from at least three insurers. Compare not just the premium but also the sum insured, the deductible amount, what riders are included, and how claims are processed. Some companies handle claims within 7 to 14 days. Others can take months. Ask about the claims process upfront. A cheap policy with terrible claims service is not actually cheap when you need it.

Also, verify that your policy covers the replacement cost of your contents, not just the depreciated value. A sofa you bought for 30,000 baht three years ago might only be valued at 10,000 baht under a depreciated policy. Replacement cost coverage means you get enough to buy a comparable new sofa. This distinction matters more than most landlords realize.

Do Not Forget to Tell Your Insurer the Unit Is Rented Out

This is a mistake that catches landlords off guard. Many people buy a homeowner's insurance policy without disclosing that the property is rented to a third party. If you file a claim and the insurer discovers the unit was being used as a rental, they can deny your claim entirely. The policy might be void.

Imagine owning a unit at Noble Revolve Ratchada near MRT Thailand Cultural Centre. You bought a basic fire and property policy when you first purchased the condo as your own home. Later, you moved out and started renting it at 14,000 baht per month. But you never updated your insurance. A burst pipe floods the unit. You file a claim. The adjuster visits, sees a tenant living there, checks the lease agreement, and flags the policy as misrepresented. Claim denied.

Always declare the rental use of your condo when purchasing or renewing insurance. The premium difference between an owner-occupied policy and a landlord policy is usually minimal, often just a few hundred baht per year. It is absolutely not worth the risk of voiding your coverage to save that small amount.

Owning a rental condo in Bangkok can be a great source of passive income, but only if you protect that income from unexpected disasters. A comprehensive insurance policy costing 3,000 to 5,000 baht per year is one of the best investments you can make as a landlord. It costs less than a single night out on Sukhumvit and can save you hundreds of thousands of baht when things go wrong. Take an afternoon, get quotes, read the fine print, and make sure your investment is properly covered. And if you are looking for tenants for your insured, well-maintained condo, list it on superagent.co to connect with quality renters searching for their next home in Bangkok.

You bought a condo near BTS Thong Lo as an investment. You spent 4.5 million baht on a one-bedroom unit at The Lofts Ekkamai, renovated the kitchen, added nice furniture, and listed it for rent at 28,000 baht per month. Within two weeks, a tenant moved in. Everything felt great. Then three months later, a pipe burst inside the wall, flooded the unit, destroyed the wooden flooring, and ruined the tenant's laptop. The repair bill came to 180,000 baht. Your tenant wanted compensation. Your juristic person said the pipe was inside your unit, so it was your responsibility. And you had zero insurance. This is the scenario nobody thinks about until it happens. If you own a rental condo in Bangkok, insurance is not optional. It is one of the smartest, cheapest protections you can buy. Let's break down exactly what kind of insurance you need and why.

Why Most Bangkok Condo Landlords Skip Insurance

Here is the honest truth. Most condo owners in Thailand do not buy insurance for their rental units. They assume the building's master insurance policy covers everything. It does not. The juristic person's policy typically covers common areas like lobbies, pools, elevators, and the building's structural elements. It rarely covers anything inside your individual unit.

Think about a building like Life Asoke Hype near MRT Phetchaburi. The juristic office maintains insurance for the entire building structure, but if a fire starts in your kitchen because of a faulty electrical outlet, you are on the hook for damages inside your four walls. Your tenant's belongings, your furniture, the repaint, the new flooring. All of it comes out of your pocket.

According to CBRE Thailand, the average rental yield for condos in central Bangkok sits between 3.5% and 5.5% annually. One uninsured incident can wipe out two or three years of rental income. That is a risk no serious investor should take.

The Three Types of Insurance Every Rental Condo Owner Should Know

Insurance in Thailand for residential property is not as complicated as people think. There are essentially three categories that matter for landlords. Understanding the differences will save you from buying the wrong policy or, worse, buying nothing at all.

The first is fire insurance, which is the most basic. In Thailand, fire insurance policies are standardized by the Office of Insurance Commission (OIC) and cover fire, lightning, and explosion. Premiums are very affordable, often under 1,000 baht per year for a condo valued at 3 to 5 million baht. But fire insurance alone is limited. It does not cover water damage, theft, or third-party liability.

The second type is comprehensive property insurance, sometimes called all-risk or multi-peril insurance. This is the one most landlords should seriously consider. It covers fire, flooding, burst pipes, storm damage, theft, and sometimes even damage caused by tenants. For a rental condo in a building like Ideo Mobi Sukhumvit near BTS On Nut, renting at around 15,000 to 20,000 baht per month, a comprehensive policy might cost between 2,500 and 5,000 baht per year. That is less than one week of rental income for a full year of coverage.

The third type is liability insurance. This is the one almost nobody buys, but it can be the most important. Imagine your air conditioning unit leaks and damages the ceiling of the unit below yours. Or your tenant's guest slips on your wet bathroom floor and breaks a wrist. Liability insurance covers claims made against you as the property owner. Some comprehensive policies include basic liability coverage. Others require a separate rider.

What Does a Typical Policy Actually Cover?

Let's get specific. Say you own a one-bedroom condo at Aspire Sukhumvit 48 near BTS Phra Khanong. You rent it out furnished at 18,000 baht per month. You buy a comprehensive property insurance policy for 3,200 baht per year. Here is what that policy would typically cover and not cover.

| Coverage Area | Typically Covered | Usually Not Covered | Estimated Annual Premium Range |

|---|---|---|---|

| Fire and Explosion | Yes, including damage to structure and contents | Arson by the owner | 800 to 1,200 THB |

| Water Damage (burst pipes, leaks) | Yes, sudden and accidental | Gradual seepage or poor maintenance | Included in comprehensive |

| Flooding from Natural Events | Sometimes, with a specific rider | Often excluded in standard policies | 500 to 2,000 THB add-on |

| Theft and Burglary | Yes, with forced entry evidence | Theft by tenant or household member | Included in comprehensive |

| Tenant Damage (intentional) | Rarely covered | Deliberate destruction by tenant | Separate landlord policy needed |

| Third-Party Liability | Yes, if included or added as rider | Professional or business liability | 500 to 1,500 THB add-on |

| Loss of Rental Income | Yes, in premium policies | Vacancy due to market conditions | 1,000 to 3,000 THB add-on |

The key takeaway from this table is that a comprehensive policy costing 2,500 to 5,000 baht per year covers the most common risks a Bangkok landlord faces. That is roughly 0.07% to 0.1% of a condo's value. Compare that to the potential cost of a single water damage incident, which can easily run 100,000 baht or more, and the math is obvious.

Flooding Risk and Why Location Matters for Your Premium

Bangkok has a complicated relationship with water. The city sits barely above sea level, and certain neighborhoods flood more than others. If your rental condo is in a low-lying area like parts of Soi Lat Phrao or near the Chao Phraya river, your insurance premium for flood coverage will be higher, sometimes significantly.

Consider this scenario. You own a studio at a riverside condo like Supalai River Resort near BTS Saphan Taksin. The views are gorgeous, the rent is solid at around 12,000 to 16,000 baht per month, but the flood risk is real. During the 2011 floods, riverside properties took serious damage. Insurers remember this. A flood rider for a riverside condo might cost 2,000 to 4,000 baht per year, while the same rider for a unit at a high-rise on Sukhumvit Soi 24 might be half that.

According to data referenced by Knight Frank Thailand, properties in flood-prone zones can see insurance premiums 30% to 60% higher than comparable units in elevated, well-drained areas. This is worth factoring into your investment calculations, especially if you are comparing rental yields across different neighborhoods.

What About Tenant Damage and the Security Deposit?

This is where most landlords feel the most frustration. Your tenant moves out after a one-year lease at a condo like Rhythm Sukhumvit 36-38 near BTS Thong Lo. You walk in and find cigarette burns on the sofa, a cracked bathroom mirror, stains all over the curtains, and a missing microwave. The security deposit was two months at 25,000 baht per month, so you have 50,000 baht to work with. But the actual repair and replacement cost is 75,000 baht.

Talk to us about renting

Share your details and keep reading — we’ll get back to you.

Standard property insurance does not cover intentional tenant damage. This is a gap that most policies explicitly exclude. Some Thai insurers now offer landlord-specific policies that cover tenant damage, but they are still uncommon and tend to carry higher premiums and deductibles. The more practical approach for most Bangkok landlords is to combine a solid comprehensive insurance policy with a well-drafted lease agreement that clearly outlines the tenant's responsibilities.

Your lease should include a detailed inventory checklist with photos, signed by both parties at move-in. This is your best protection against tenant damage disputes, even more effective than insurance in most cases. Use the security deposit strategically and document everything.

How to Choose the Right Insurance Provider in Thailand

Thailand has dozens of insurance companies, but not all of them handle condo property insurance well. The major players for residential property insurance include Viriyah Insurance, Bangkok Insurance, Dhipaya Insurance, and Muang Thai Insurance. All four are well-established, financially stable, and regulated by the OIC.

Here is a real-world example of how to approach this. Say you own two rental condos, a one-bedroom at Ideo Q Siam near BTS Ratchathewi renting at 22,000 baht per month and a studio at Lumpini Park Rama 9 near MRT Rama 9 renting at 11,000 baht per month. You would want comprehensive property insurance for both units. You can often get a discount by insuring multiple properties with the same company.

Start by requesting quotes from at least three insurers. Compare not just the premium but also the sum insured, the deductible amount, what riders are included, and how claims are processed. Some companies handle claims within 7 to 14 days. Others can take months. Ask about the claims process upfront. A cheap policy with terrible claims service is not actually cheap when you need it.

Also, verify that your policy covers the replacement cost of your contents, not just the depreciated value. A sofa you bought for 30,000 baht three years ago might only be valued at 10,000 baht under a depreciated policy. Replacement cost coverage means you get enough to buy a comparable new sofa. This distinction matters more than most landlords realize.

Do Not Forget to Tell Your Insurer the Unit Is Rented Out

This is a mistake that catches landlords off guard. Many people buy a homeowner's insurance policy without disclosing that the property is rented to a third party. If you file a claim and the insurer discovers the unit was being used as a rental, they can deny your claim entirely. The policy might be void.

Imagine owning a unit at Noble Revolve Ratchada near MRT Thailand Cultural Centre. You bought a basic fire and property policy when you first purchased the condo as your own home. Later, you moved out and started renting it at 14,000 baht per month. But you never updated your insurance. A burst pipe floods the unit. You file a claim. The adjuster visits, sees a tenant living there, checks the lease agreement, and flags the policy as misrepresented. Claim denied.

Always declare the rental use of your condo when purchasing or renewing insurance. The premium difference between an owner-occupied policy and a landlord policy is usually minimal, often just a few hundred baht per year. It is absolutely not worth the risk of voiding your coverage to save that small amount.

Owning a rental condo in Bangkok can be a great source of passive income, but only if you protect that income from unexpected disasters. A comprehensive insurance policy costing 3,000 to 5,000 baht per year is one of the best investments you can make as a landlord. It costs less than a single night out on Sukhumvit and can save you hundreds of thousands of baht when things go wrong. Take an afternoon, get quotes, read the fine print, and make sure your investment is properly covered. And if you are looking for tenants for your insured, well-maintained condo, list it on superagent.co to connect with quality renters searching for their next home in Bangkok.

Share this article

Properties you may like

![[For Rent] BUILDING I Quach House Phrom Phong I 1st-6th Floor I 100,000-135,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F1976%2F333d3ec9-941e-431d-8a0c-68b9d7bdbc41-1000002210.jpg&w=3840&q=75)

฿135,000

[For Rent] BUILDING I Quach House Phrom Phong I 1st-6th Floor I 100,000-135,000THB/mo

Townhouse![[For Rent] CONDO I Waterford Diamond Sukhumvit 30/1 I 3 Beds I 3 Baths I 65,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2049%2Fa78ddba5-043d-459a-97eb-4f80a7bf7d1a-8f2dc5c8-f220-47ae-b027-7deab6c6666b-media.jpg&w=3840&q=75)

฿65,000

[For Rent] CONDO I Waterford Diamond Sukhumvit 30/1 I 3 Beds I 3 Baths I 65,000THB/mo

Phrom Phong

Condo![[For Rent] HOUSE I Centro Vibhavadi I 4 Beds I 3 Baths I 80,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2048%2F7bcb9b3f-6bca-4615-8451-eb71e0910ecc-26-07-09-15-10-22-747_deco.jpg&w=3840&q=75)

฿80,000

[For Rent] HOUSE I Centro Vibhavadi I 4 Beds I 3 Baths I 80,000THB/mo

House![[For Rent] CONDO I RHYTHM Sathorn I 1 Bed I 1 Bath I 20,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2045%2Fcd83dbf6-1fcd-43e1-9788-a9f9ef92106c-img_2861.jpg&w=3840&q=75)

฿20,000

[For Rent] CONDO I RHYTHM Sathorn I 1 Bed I 1 Bath I 20,000THB/mo

Condo![[For Rent] TOWNHOME I Gravitia Rama 2-Thakam I 3 Beds I 3 Baths I 35,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2046%2F3a6c0105-9e14-456f-8fde-b8a52d7cec89-line_album_-531_260714_16.jpg&w=3840&q=75)

฿35,000

[For Rent] TOWNHOME I Gravitia Rama 2-Thakam I 3 Beds I 3 Baths I 35,000THB/mo

Townhouse![[For Rent & Sale] CONDO I KHUN by YOO I 2 Beds I 2 Baths I Rent 130,000THB/mo - Sale 37,000,000mb THB](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2015%2Fac778d88-63d8-418e-8291-ce27e76eb87b-17227fa8597d930453882fcb8eceab768aa7d514.jpg&w=3840&q=75)

฿130,000

[For Rent & Sale] CONDO I KHUN by YOO I 2 Beds I 2 Baths I Rent 130,000THB/mo - Sale 37,000,000mb THB

Thonglor

Condo![[For Rent] CONDO I IDEO Ratchada-Huai Khwang I 2 Beds I 2 Baths I 25,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F1935%2Fac9ba95a-0ad4-4121-9287-226c06205f6f-1782609678044-61071c89.jpg&w=3840&q=75)

฿25,000

[For Rent] CONDO I IDEO Ratchada-Huai Khwang I 2 Beds I 2 Baths I 25,000THB/mo

Huai Khwang

Condo![[For Rent] HOUSE I Laddarom Rattanathibet I 4 Beds I 3 Baths I Rent 80,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F2035%2Ff8ee11b5-97d3-475e-b58b-49ebc833161e-ef77c7dc-87f5-4b5e-8a7d-0c4e41b65b6b-a34.jpg&w=3840&q=75)

฿80,000

[For Rent] HOUSE I Laddarom Rattanathibet I 4 Beds I 3 Baths I Rent 80,000THB/mo

House![[For Rent] CONDO I Life @ Sathon 10 I 1 Bed I 1 Bath I Rent 20,000THB/mo](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F1954%2F3e4ff511-b8de-40a5-894e-c8fc6777e2b0-living-room1.jpg&w=3840&q=75)

฿20,000

[For Rent] CONDO I Life @ Sathon 10 I 1 Bed I 1 Bath I Rent 20,000THB/mo

Sathorn

Condo![[For Rent&Sale] CONDO I Belle Grand Rama 9 I 2 Beds I 2 Baths I Rent 45,000THB/mo - Sale 10.7mb THB](/_next/image?url=https%3A%2F%2Fstorage.googleapis.com%2Fsuperagent-web%2Fattachments%2Flistings%2F1961%2Fef57f38f-f765-4980-a394-8c66e43efea4-line_album_27626_260701_11.jpg&w=3840&q=75)

฿45,000

[For Rent&Sale] CONDO I Belle Grand Rama 9 I 2 Beds I 2 Baths I Rent 45,000THB/mo - Sale 10.7mb THB

CondoMore like this

In Guides · Superagent EditorialHidden Costs of Renting a Condo in Bangkok Nobody Warns You AboutBangkok condo rent looks affordable until month one hits. Here are the real costs beyond the headline figure that catch most renters off guard.25 May 20261 min read

In Guides · Superagent EditorialHidden Costs of Renting a Condo in Bangkok Nobody Warns You AboutBangkok condo rent looks affordable until month one hits. Here are the real costs beyond the headline figure that catch most renters off guard.25 May 20261 min read In Guides · Superagent EditorialWhat a Long-Vacant Bangkok Condo Unit Is Actually Telling YouA Bangkok condo vacant for months signals overpricing, landlord issues, or real problems. Here is how to read the signs.25 May 20261 min read

In Guides · Superagent EditorialWhat a Long-Vacant Bangkok Condo Unit Is Actually Telling YouA Bangkok condo vacant for months signals overpricing, landlord issues, or real problems. Here is how to read the signs.25 May 20261 min read In Guides · Superagent EditorialRed Flags in a Bangkok Rental Contract to Watch Out ForBangkok rental contracts often hide risky clauses. Here are the red flags every tenant must catch before signing any lease.25 May 20261 min read

In Guides · Superagent EditorialRed Flags in a Bangkok Rental Contract to Watch Out ForBangkok rental contracts often hide risky clauses. Here are the red flags every tenant must catch before signing any lease.25 May 20261 min read In Guides · Superagent EditorialWorking Online from a Condo: How to Choose the Perfect Room for ProductivityLearn how to choose the best condo room for working online with tips on lighting, noise, and furniture setup to maximize productivity.9 May 20261 min read

In Guides · Superagent EditorialWorking Online from a Condo: How to Choose the Perfect Room for ProductivityLearn how to choose the best condo room for working online with tips on lighting, noise, and furniture setup to maximize productivity.9 May 20261 min read